Consumption and imports remained stable, indicating continued growth in the share of imported steel in the region.

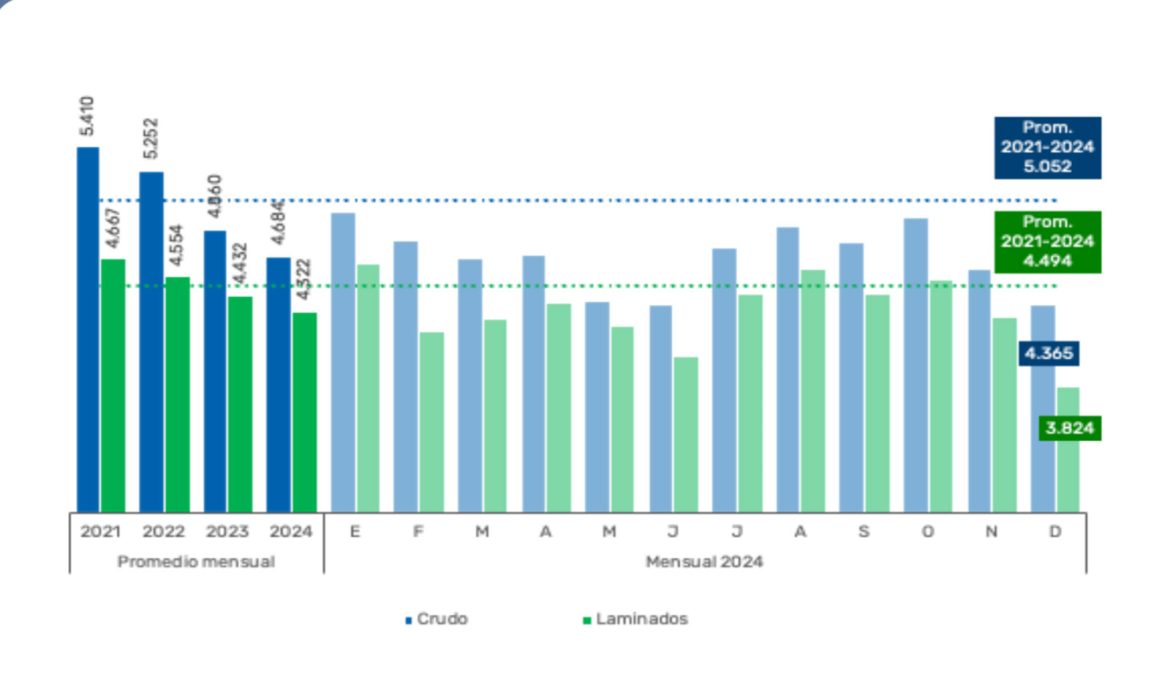

São Paulo, March 11, 2025 – According to the latest monthly report from Alacero – the Latin American Steel Association – on the evolution of production, consumption, and trade balance of the region’s industry, crude steel production in Latin America reached 56.2 million tons (Mt) in 2024, representing an annual decline (y/y) of -3.6%, marking the third consecutive drop (-2.9% in 2022 and -7.4% in 2023). The most significant decreases were recorded in Mexico, Argentina, and Chile, while Brazil, with 33.7 Mt (+5.3%), was the only country to report an increase in production.

Flat steel production totaled 51.9 million tons, with a decrease of -2.5% y/y, continuing the downward trend of recent years (-2.4% in 2022 and -2.7% in 2023). The seamless tube segment experienced the largest decline (-8.8%), followed by long steels (-5.0%). On the other hand, flat products grew by 0.7%.

The trade balance in Latin America recorded a deficit of 19.5 million tons between January and November 2024, reflecting a 4.3% increase compared to the same period in 2023. This deficit was caused by a -10.5% drop in exports, while imports remained stable, with a growing increase in purchases from China.

Apparent consumption of flat products was 67.4 million tons over the 11-month period, representing a decrease of -1.0% y/y. The performance varied greatly among the region’s countries, with declines of over -20% in Argentina, Bolivia, and Panama, which were partially offset by increases in Brazil, Colombia, Paraguay, Uruguay, and Venezuela.

Regarding the steel-consuming sectors, construction saw a growth of 1.5% y/y, although it faced declines from August to November 2024, except for Brazil. The industrial sector closed the semester with a positive performance in November 2024 (1.3% y/y), with the automotive sector standing out (5.9%), while the industrial machinery and equipment sector showed moderate growth of 0.4%. The household appliances sector, on the other hand, recorded a decrease of -1.9%.

“We closed 2024 with a decline for the third consecutive year in steel production in Latin America. However, consumption and imports remained stable, indicating that the share of imported steel continues to grow in our region. This directly impacts the competitiveness and structure of the regional value chain,” explains Ezequiel Tavernelli, Executive Director of Alacero.

The full report, with graphs, is available at:

About Alacero

The Latin American Steel Association is a non-profit civil entity that brings together the steel value chain in Latin America with the aim of promoting quality industrial employment, regional integration, technological innovation, environmental care, excellence in human resources, workplace safety, the comprehensive development of its communities, and corporate responsibility. Founded in 1959, it is composed of more than 50 producing and related companies. The region’s industry, with an annual production of 56 million tons, generates approximately 1.4 million direct and indirect jobs. Alacero represents Latin America’s steel industry in international organizations such as worldsteel, the OECD, the International Energy Agency (IEA), the UN (UNCTAD), and the IDB, advocating for the ideas and positions of its members.