In March, crude and rolled steel production in Latin America interrupted the negative trend of the last six months. Although consumption during 2025 is on the rise, the volume of imports reached the highest level -during a month of February- in the last 15 years, with an average share of imports of 40% in the apparent consumption of rolled steel.

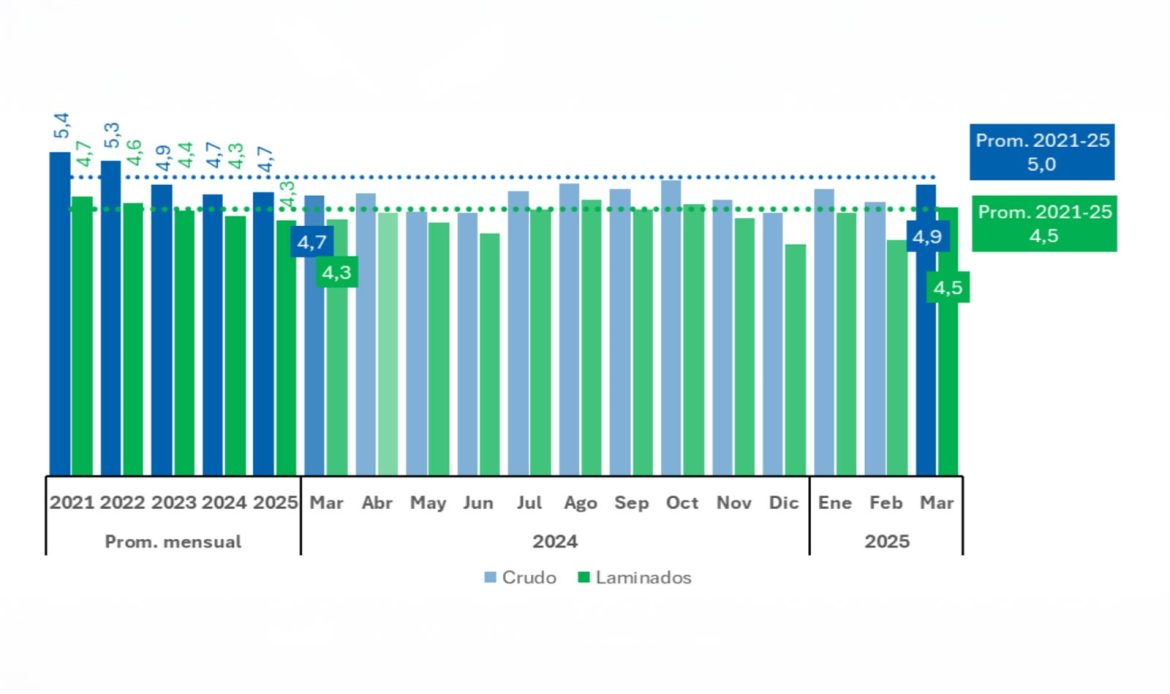

Crude steel production in LATAM reached 4.9 million tons (Mt) in March, a year-on-year increase of 3.7%. This increase reduced the accumulated drop so far this year to -1.7% compared to the same quarter of 2024. The expansion was driven by the March results in Brazil, Mexico and Argentina.

Rolled steel production reached 4.5 Mt in March, with growth in both long products (+6.6% YoY) and flat products (+3.6% YoY), which offset the decline in seamless tubes (-13.4% YoY). Although the production of rolled products improved compared to the same period of the previous year (+4.7%), the annual accumulated production remains negative (-2.5% vs. 1Q-2024).

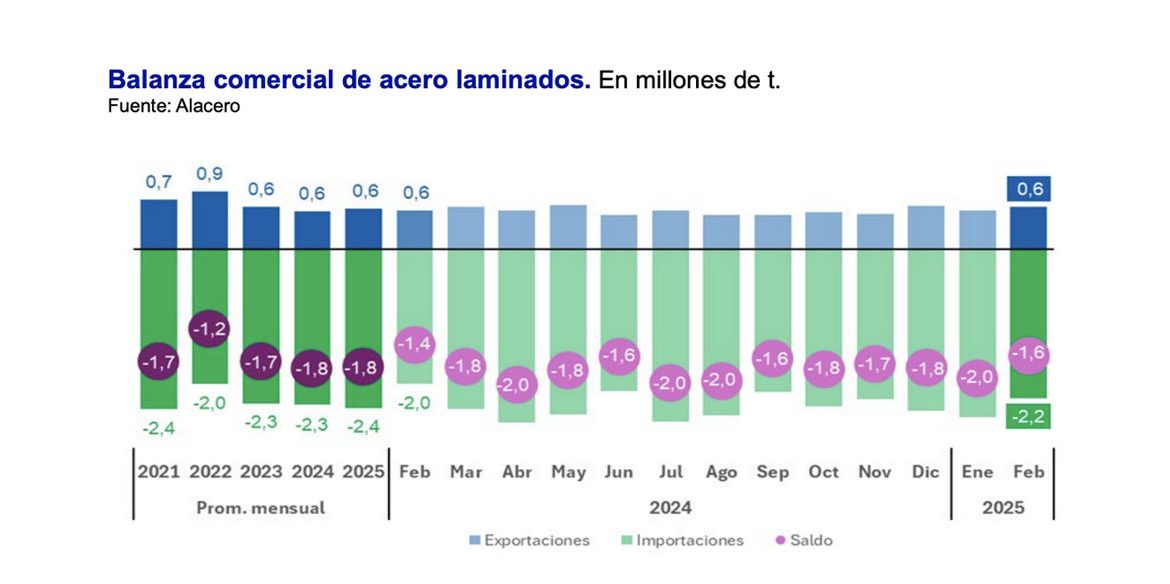

Regarding the trade balance, a deficit of 3.6 Mt was recorded in the first two months of 2025, the largest trade imbalance in the last 15 years for that period. Imports totaled a record level for February (2.2 Mt), and grew 10.3% year-on-year. Exports reached 0.6 Mt in February and advanced 8.3% year-on-year.

Apparent consumption of rolled products reached 5.7 Mt during February, up 3.4% compared to the same period of 2024. This is due to the rebound in demand in Brazil and Argentina, which helped to offset the decline in Mexico.

In relation to the value chain, steel demand sectors maintain disparity. Construction activity showed its first positive rate in six months, and there was moderate growth in machinery and automotive production.

Most of the steel demanding sectors presented increases in relation to the same period of the previous year, with an expansion in the construction activity of 5.4% in relation to March 2024, and the industry with an increase of 3.3% in comparison with March of the previous year).

To see the full report: