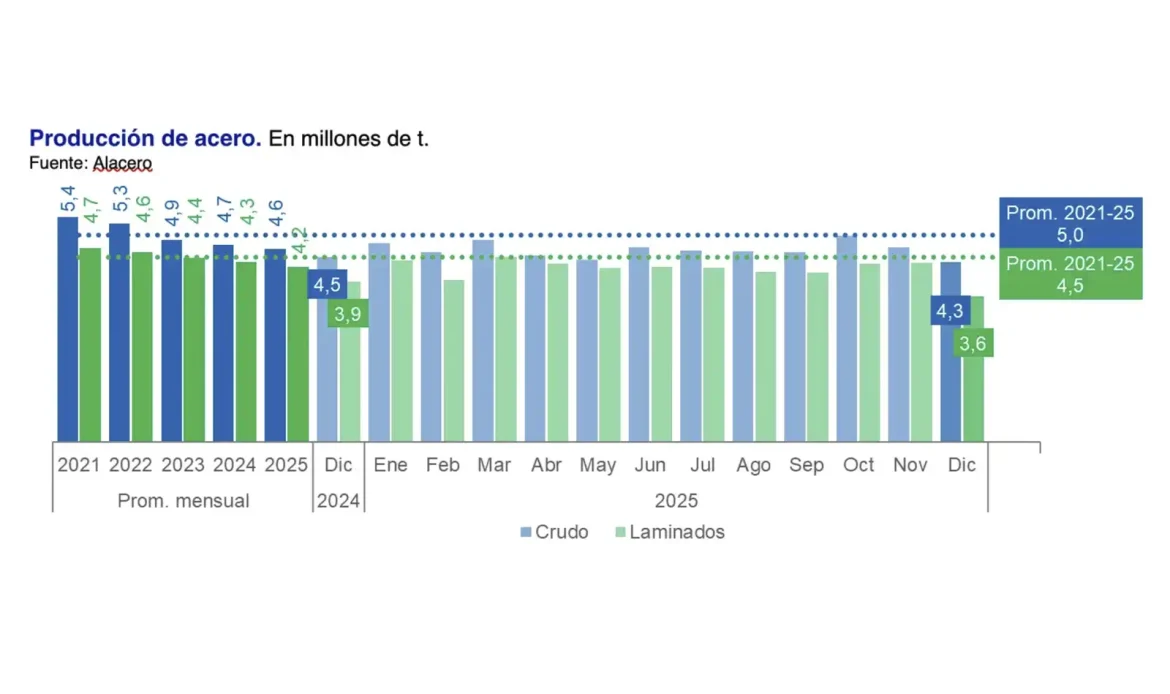

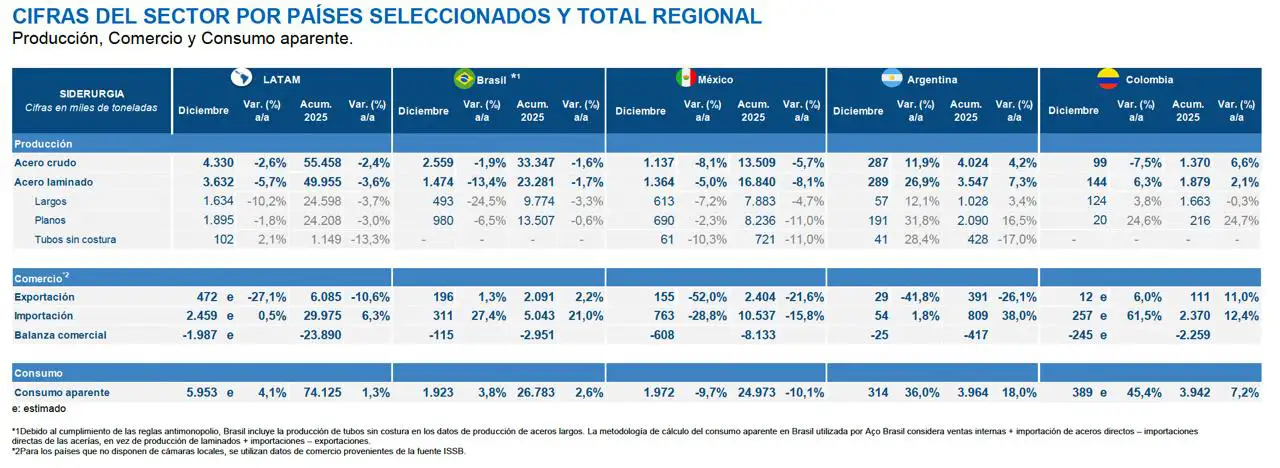

In December 2025, the sector’s performance continued the weakness seen in recent months, with production down (4.3 Mt, −2.6% year-over-year for crude steel and 3.6 Mt, −5.7% year-over-year, of rolled steel), rising imports (+0.5% y/y, 2.5 Mt), a regional trade deficit (-2.0 Mt), and growing apparent consumption (6.0 Mt, +4.1% y/y).

Thus, although apparent consumption is projected to grow by +1.3% y/y in 2025 (74 Mt), production is set to contract for the fourth consecutive year—with 55.5 Mt of crude steel (-2.4% y/y) and 50. 0 Mt of rolled steel (-3.6% y/y)—a situation comparable only to production levels during the pandemic. Rounding out the negative outlook is the record-high share of foreign purchases in apparent consumption at 40.4%—the highest in the historical series—totaling an import volume of 30 Mt in 2025 (+6.3% y/y).

In rolled steel production, performance varied by product: flat products declined by −3.0% year-over-year, and long products decreased by −3.7% year-over-year on a year-to-date basis, while seamless tubes recorded the sharpest contraction of the year, with a drop of −13.3% year-over-year.

In contrast to production, apparent consumption of rolled products showed a slight increase in 2025. It reached 74.1 Mt for the full year, with year-over-year growth of +1.3%. At the country level, Argentina led the recovery with a strong increase of +18.0% year-over-year, followed by Colombia (+7.2% year-over-year) and Brazil (+2.6% year-over-year), while Mexico recorded a significant contraction of −10.1% year-over-year for the year to date.

In 2025, imports reached a historic high of 30.0 Mt, representing a +6.3% year-over-year increase compared to the previous year. In terms of annual imports by country, Mexico closed 2025 with 10.5 Mt (-15.8% year-over-year) and Brazil with 5 Mt (+21%). At the same time, exports closed at 6.1 Mt (−10.6% YoY), resulting in a cumulative regional trade deficit of −23.9 Mt, the largest negative balance on record.

On the demand side, the end of 2025 showed mixed trends. Construction managed to close the year with a slight increase (+0.4% year-over-year). Among industrial sectors, Machinery posted growth of +2.7% year-over-year, while Household Goods contracted by −2.9% year-over-year. The Automotive sector ended the year with a weak performance (+0.7% year-over-year), reflecting an industrial landscape that remains fragile.