During 2024 and early 2025, crude and rolled steel production in Latin America continues to contract. Rolled steel consumption in the region shows a slight decline, affected by reduced demand. The trade balance shows its largest deficit since 2011, with further drops in exports and imports near record levels.

In the first month of 2025, crude and rolled steel production in Latin America continued to decline, reflecting the challenges faced by the sector.

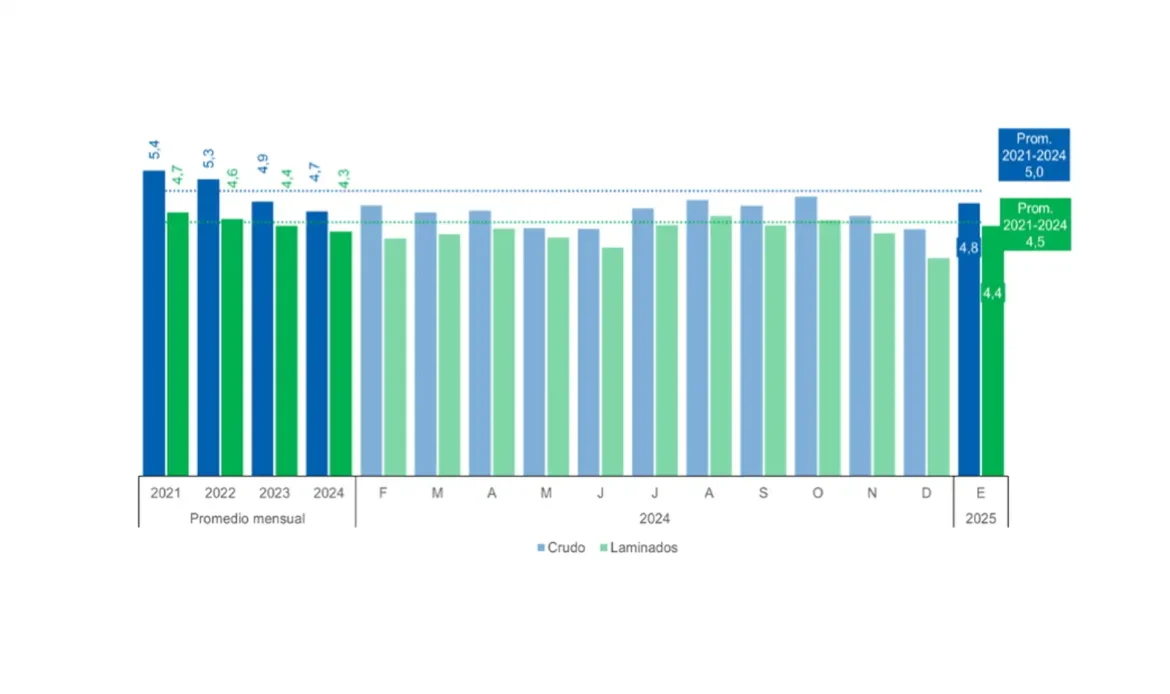

Crude steel production reached 4.8 million tons (Mt) in January 2025, marking a -3.0% year-over-year decrease compared to January 2024. Poor performance in Argentina and Mexico outweighed growth in Colombia and Brazil, leading to a fourth consecutive contraction.

Rolled steel production stood at 4.4 Mt in January 2025, a decline of -4.6% compared to the same month of the previous year. The most significant drop was seen in seamless tubes (-23.4% y/y), followed by flat products (-4.3% y/y) and long products (-3.8% y/y). Production decreased in the region’s three largest producers — Mexico, Argentina, and Brazil. In Brazil’s case, this marks the first annual drop since May 2024.

Regarding annual figures, in 2024, crude steel production in Latin America totaled 56.2 Mt, while rolled steel production reached 51.9 Mt.

In 2024, the trade balance recorded its largest deficit since 2011, with a further decline in exports and imports nearing record levels.

The negative balance ended at -21.3 Mt, slightly higher than in 2023 (-20.2 Mt). Imports reached 28.2 Mt, representing a 1.1% increase from the previous year and just 2.6% below the all-time high (29.0 Mt in 2021).

Exports, on the other hand, totaled 6.9 Mt (-10.4% y/y), marking their lowest volume in the last 14 years.

In 2024, rolled steel consumption in Latin America declined slightly, affected by lower regional demand.

Apparent rolled steel consumption totaled 73.2 Mt in 2024, showing a -0.7% drop compared to 2023. Last year’s decline was due to reduced demand in Argentina and Mexico, which was not offset by growth in Peru, Colombia, and Brazil.