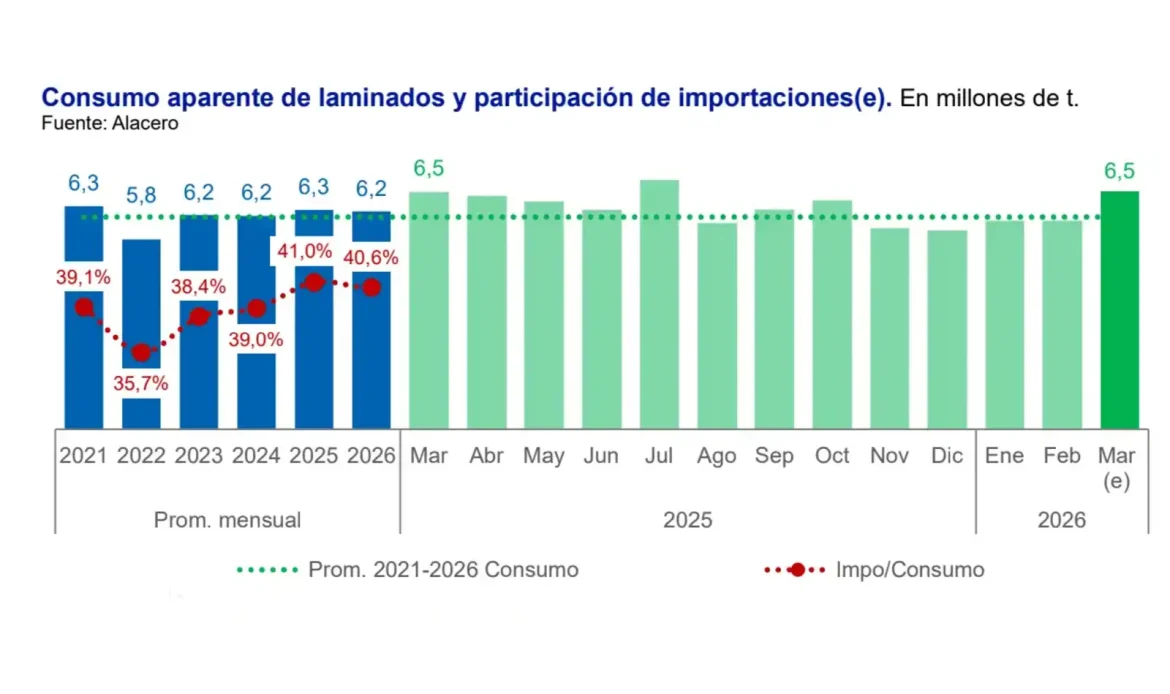

In March, the sector showed some disparity: crude steel production increased, while rolled steel production declined. Both exports and imports registered decreases, whereas apparent consumption remained relatively stable. Despite the monthly decrease in imports, imported steel still accounted for nearly 40% of regional apparent consumption in the first quarter, maintaining a strong presence in the Latin American steel market.

Regarding production in the region, crude steel production reached 4.9 Mt in March, representing a 1.1% year-over-year increase, and totaled 13.9 Mt during the first quarter, marking a 1.9% decrease compared to the same period last year. Meanwhile, rolled steel production showed a -2.2% year-over-year change, with 4.4 Mt produced during the third month of the year, ending the quarter at 12.6 Mt (-1.8% year-over-year). Apparent consumption of rolled steel reached 6.5 Mt, remaining virtually unchanged from the previous year (+0.1%).

Meanwhile, imports totaled 2.5 Mt in March, reflecting a year-over-year decline of -8.6%. Year-to-date, they reached 7.6 Mt, with a contraction of -1.2% compared to the same period last year. Significant declines were observed in Chile, Mexico, and Brazil. However, in the year-to-date figures for 2026 by country, import growth stood out in Brazil (+11.4% y/y) and Colombia (+16.3% y/y), while imports declined in Mexico (-18.1% y/y) and Argentina (-2.6% y/y).

Exports totaled 0.54 Mt, down 13.4% from March 2025, and reached 1.7 Mt year-to-date (down 11.7% year-over-year). At the country level, in the first quarter of the year, only Brazil’s exports grew, while those of Colombia, Mexico, and Argentina fell. As a result, the regional balance was in deficit by −1.9 Mt in the third month of the year and accumulated a deficit of -5.9 Mt in Q1 2026.

In the first months of the year, steel-consuming sectors have not rebounded, and their performance remains largely negative in the first months of 2026. The exceptions were the automotive sector —which increased by +1.1% year-over-year in the first four months of the year— and construction—which remained at a level similar to that of the first quarter of the previous year.